Skip to content

Skip to content Save Big During Tax Season

- Immediate Access

- No set-up fees

- No Inspection

- Instant results

- Safe and secure

Save Big During Tax Season: A Comprehensive Guide for Landlords

Tax season presents an opportunity for landlords to maximize savings and optimize rental income through careful planning and informed decisions. To help you save big during tax season and get the most out of your tax return, we’ve compiled essential tips and advice tailored for rental property owners. From taking advantage of tax deductions to staying compliant with recent tax laws, this guide is designed to ensure that you minimize tax liabilities while maintaining a profitable rental business.

Key Takeaways

- Leverage Tax Deductions: Learn how specific deductions can reduce your tax burden.

- Utilize COVID-19 Resources: Discover relevant resources that assist landlords in the wake of the pandemic.

- Practice Effective Record-Keeping: Maintain organized records to streamline the tax filing process.

- Understand the Tax Cuts and Jobs Act (TCJA): Explore key changes that may benefit landlords.

- File Taxes Correctly: Learn how to file your taxes based on your rental business setup.

By implementing these strategies, landlords can maximize tax refunds and ensure compliance with current tax regulations

1. Top Tax Deductions for Landlords

Understanding and utilizing tax deductions can significantly reduce the amount you owe during tax season. Here are the top deductions that landlords should consider:

Depreciation for Rental Real Estate

One of the most valuable deductions available to landlords is depreciation, allowing you to recover the cost of your property over time. The IRS permits you to deduct a portion of your rental property’s value each year, reducing your taxable income.

- Key Insight: The depreciation period for residential real estate is typically 27.5 years. It’s essential to keep accurate records of the property’s purchase price and improvements to calculate this deduction properly.

Insurance Premiums

Did you know that most insurance premiums related to your rental property are deductible? This includes coverage such as landlord liability, fire, and flood insurance. Protecting your investment through insurance while reducing your tax liability is a win-win.

Repairs

Ordinary repairs made to your rental property—such as fixing a leaky roof, repainting, or repairing gutters—can be deducted in the year the expense was incurred. However, it’s crucial to differentiate between repairs and improvements. While repairs are deductible, improvements must be depreciated over time.

2. COVID-19 Resources for Landlords

The COVID-19 pandemic introduced significant challenges for landlords, from navigating eviction moratoriums to dealing with financial instability. Although many pandemic-related relief measures have ended, there are still resources available to assist landlords:

Rental Assistance Programs

Many landlords have benefited from COVID-19 relief packages, which provided billions in rental assistance. Although these programs have scaled back, understanding available resources is still essential. For example, Benefits.gov offers a wealth of information on federal and state relief efforts.

Impact on Rental Income

According to the Harvard Center for Housing Studies, small landlords received only about 50% of their expected rental income during the height of the pandemic. Tax season provides an opportunity to recover some of these losses through deductions related to missed rent or other relief measures.

3. Essential Records Landlords Should Keep for Tax Season

Maintaining thorough records is vital for maximizing tax savings and avoiding issues with the IRS. Here’s a breakdown of essential documents:

Long-Term Records

- Leases and rental agreements: Keep copies for all properties.

- Legal documents: Include inspection reports, court appearances, or fines.

- Permits and insurance policies: Maintain a record of any permits and insurance coverage relevant to the property.

- Loan documents: Retain mortgage or business loan records.

Short-Term Records

- Expense receipts: Include receipts for repairs, utilities, and mortgage interest.

- Rent payment records: Track all rent payments received and any outstanding balances.

Expert Tip: Using digital tools like cloud-based storage solutions or property management software can simplify record-keeping and ensure everything is organized for tax season.

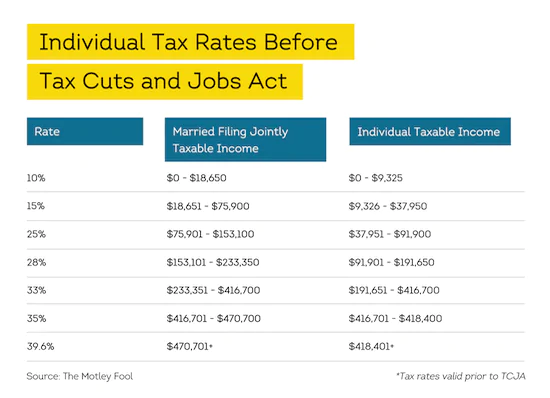

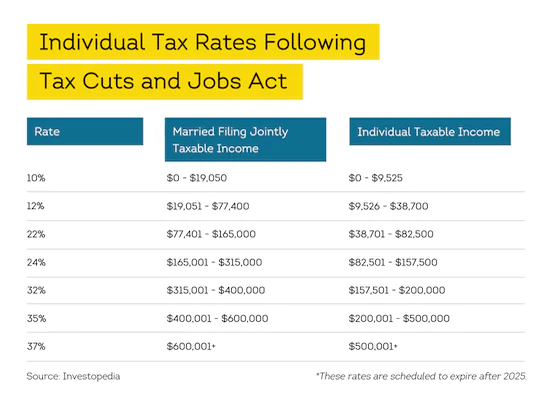

4. What Landlords Should Know About the Tax Cuts and Jobs Act (TCJA)

The Tax Cuts and Jobs Act (TCJA) introduced several changes that impact landlords. Here are some highlights:

Lower Individual Tax Rates

Many landlords report rental income as part of their individual tax returns. Under the TCJA, individual tax rates have been lowered, which could mean a smaller tax bill for property owners who report income on their personal returns.

Pass-Through Tax Deduction

Landlords who operate their rental properties through pass-through entities such as LLCs or partnerships may qualify for a 20% deduction on their net rental income. This deduction is particularly advantageous for property owners who meet the income qualifications.

Expanded Section 179 Expensing

Landlords can now deduct the cost of personal property used in rental activities, such as appliances, laundry equipment, or furniture, thanks to expanded expensing limits under Section 179. The limit was increased from $500,000 to $1,000,000, which allows for more immediate write-offs of purchases.

The TCJA reduces these individual rates until 2025, at which point they’ll expire. As of 2022, the individual tax rates are as follows:

5. Filing Taxes Based on Ownership Status

The way you file your taxes depends largely on how your rental property is owned. Here are key details to keep in mind:

Individually Owned Rental Property

- Schedule E: Use IRS Schedule E to report rental income and expenses if you own the property individually or with a co-owner.

Business-Owned Rental Property

- Form 8825: If your rental property is owned through an entity such as an LLC or partnership, report your income using IRS Form 8825.

Filing taxes correctly ensures that you remain compliant while optimizing potential deductions.

Conclusion: Maximizing Your Tax Return as a Landlord

Filing taxes as a landlord doesn’t have to be overwhelming. By leveraging key deductions, staying informed about relevant tax laws, and keeping accurate records, you can save big during tax season. Whether you’re a seasoned property owner or a new landlord, taking proactive steps now will ensure that you maximize your returns and maintain a profitable rental business.

Final Thought: Consider consulting a tax professional to ensure you’re taking full advantage of every deduction and tax break available. The investment in professional advice can pay off with significant savings.